Trusted By 65,000 Professionals

Protect Your Client Reputation.

Insights for Professional Firms.

.png)

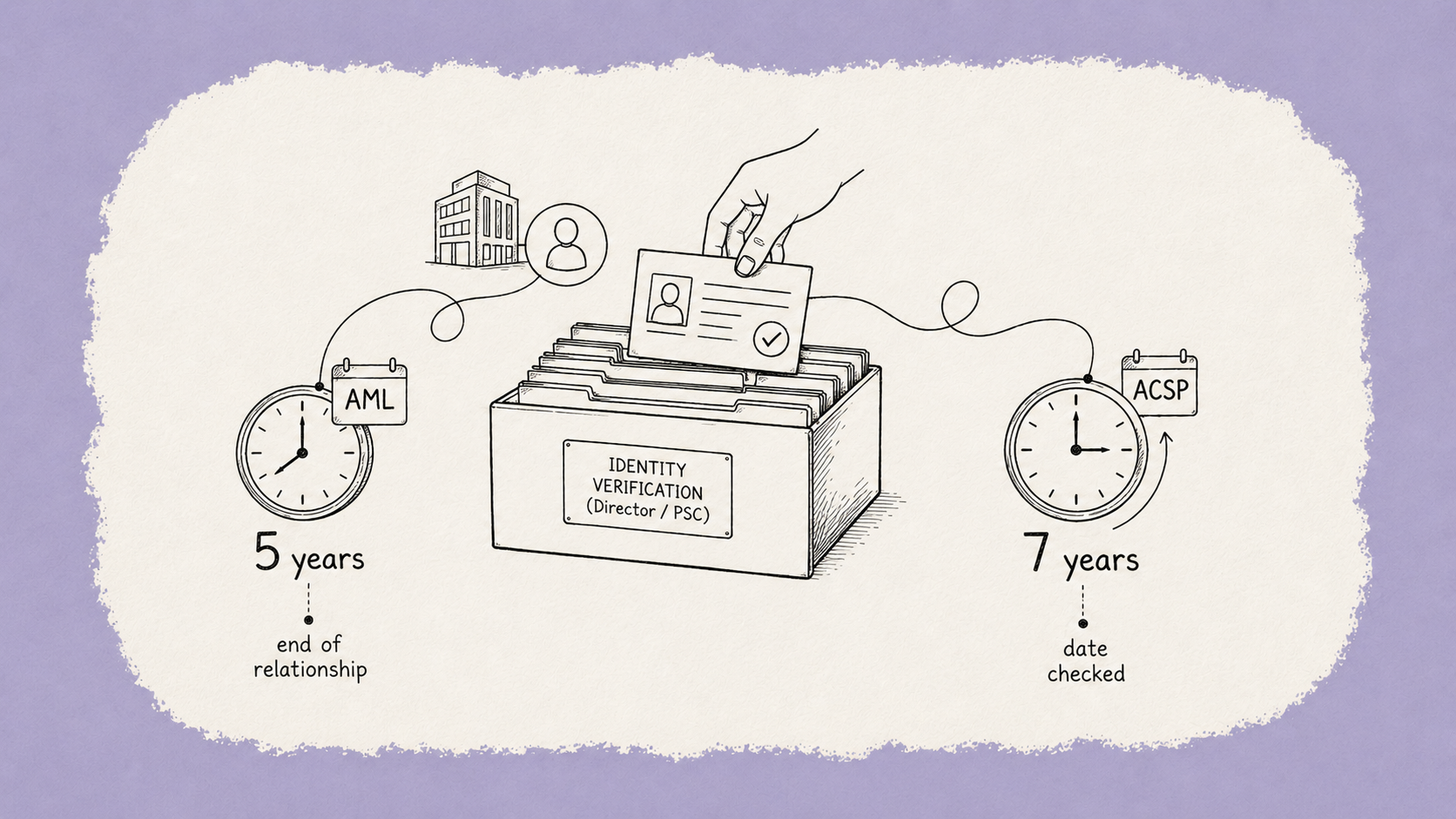

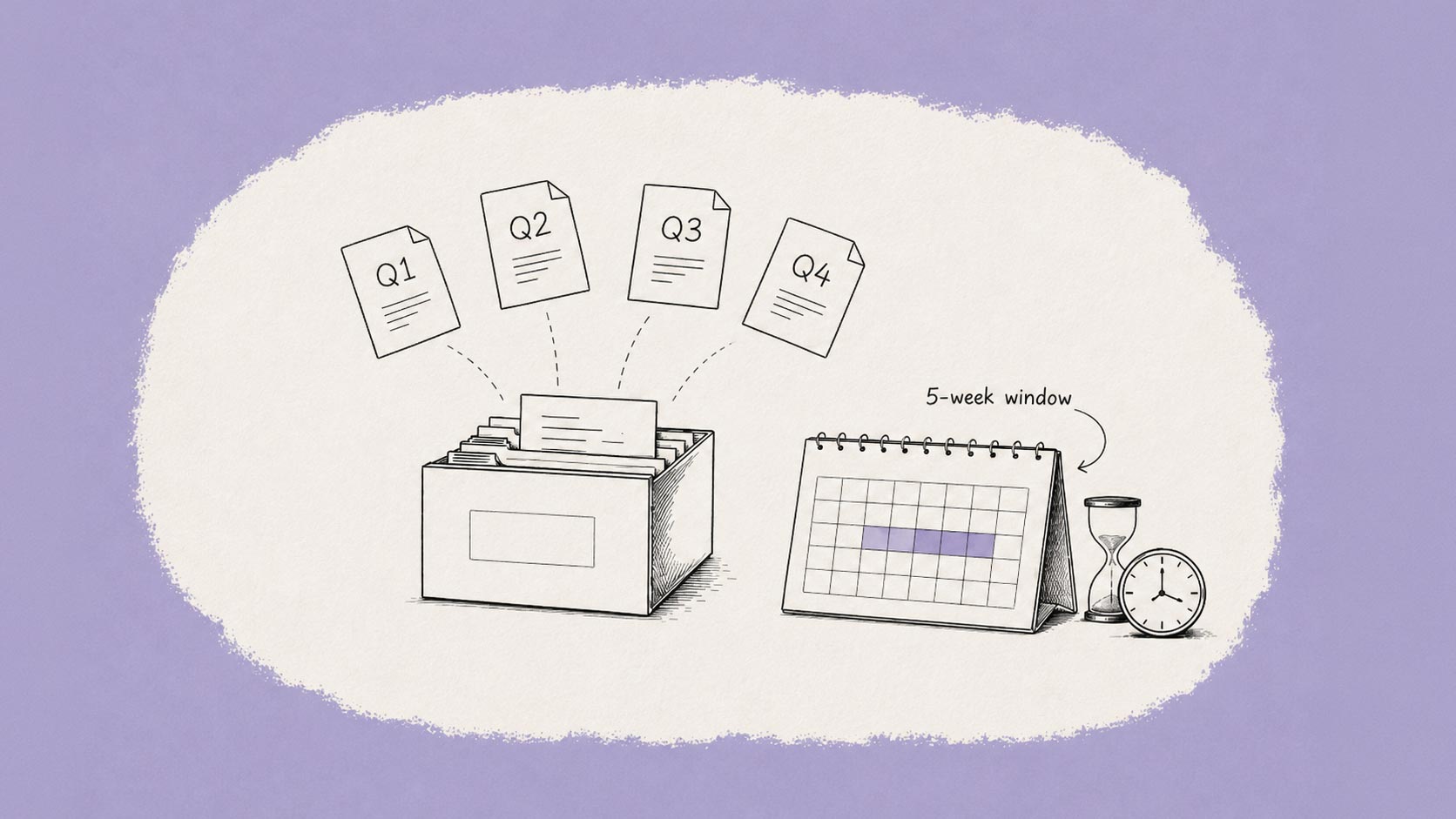

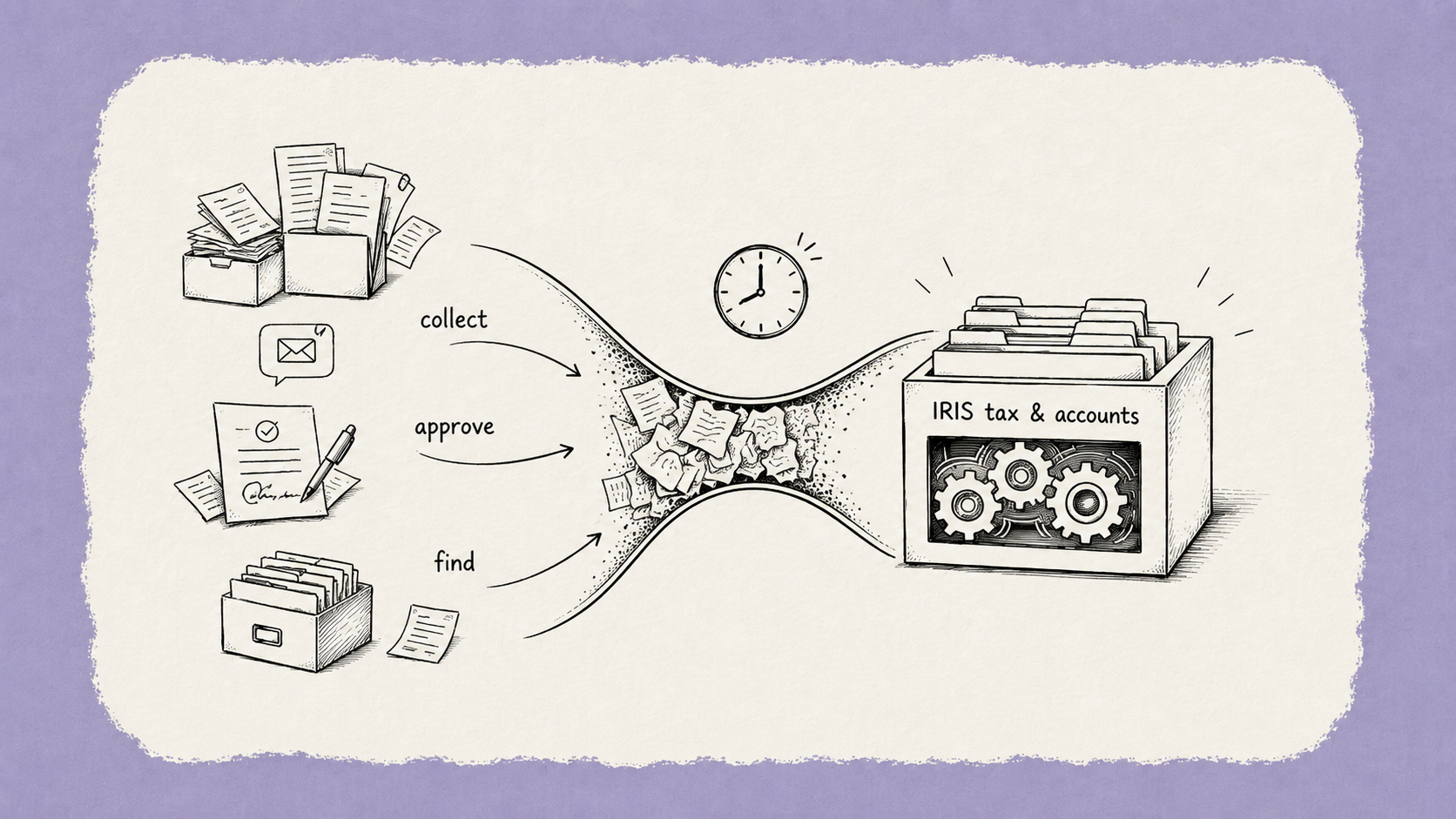

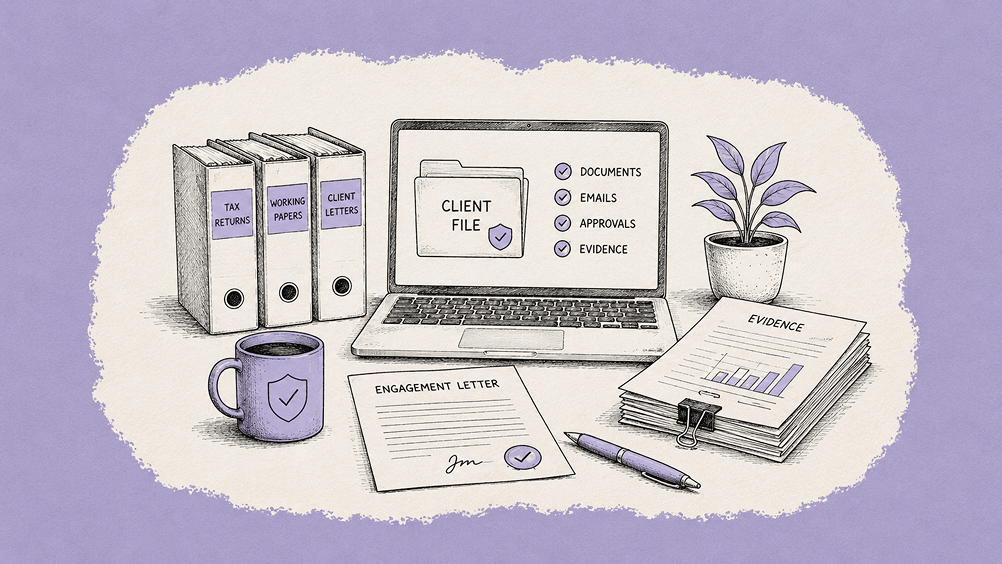

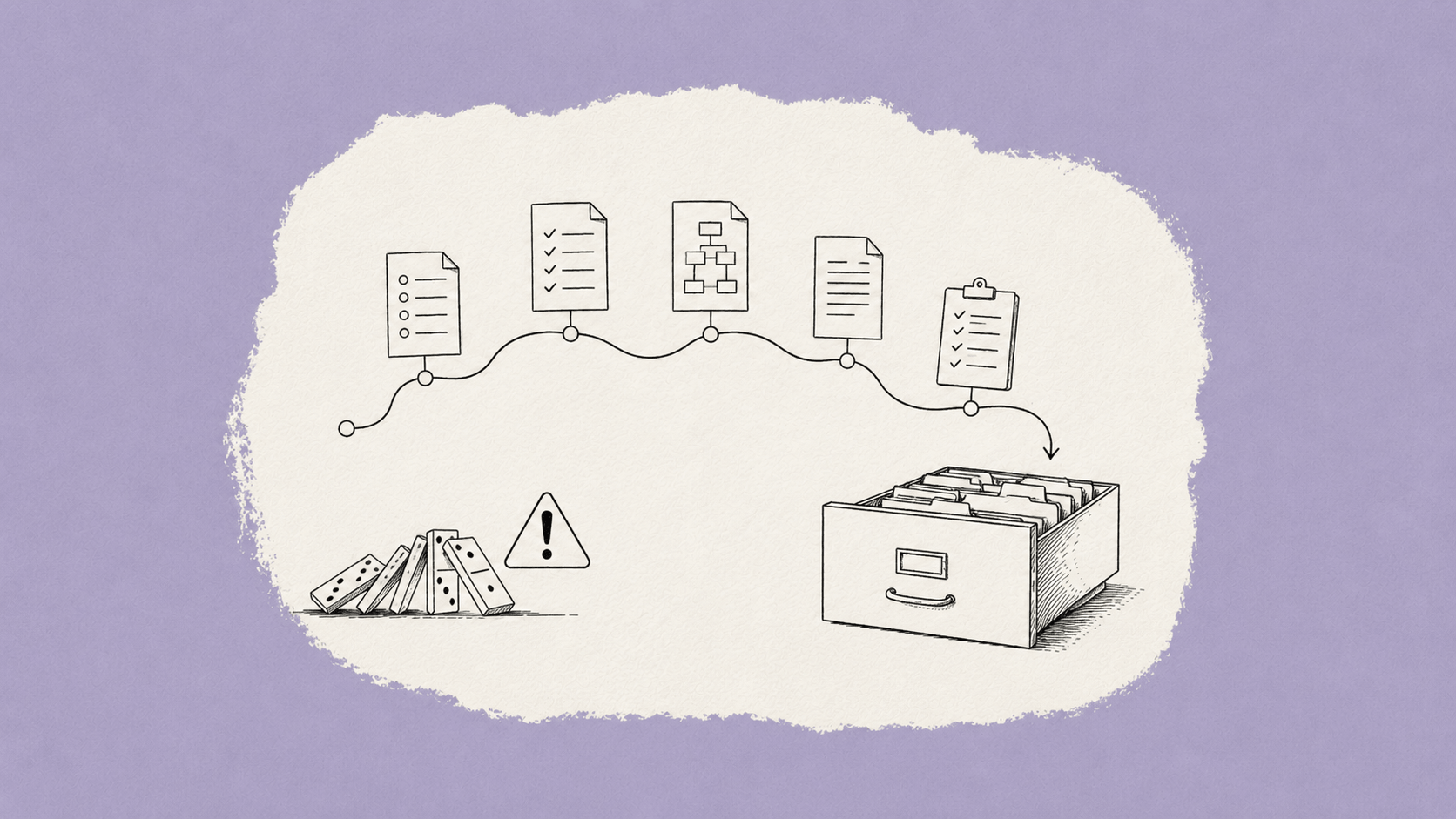

Keep Every Client File Defensible — Without Slowing Work Down.

Book a demo

Trusted By 65,000 Professionals

Book a demo

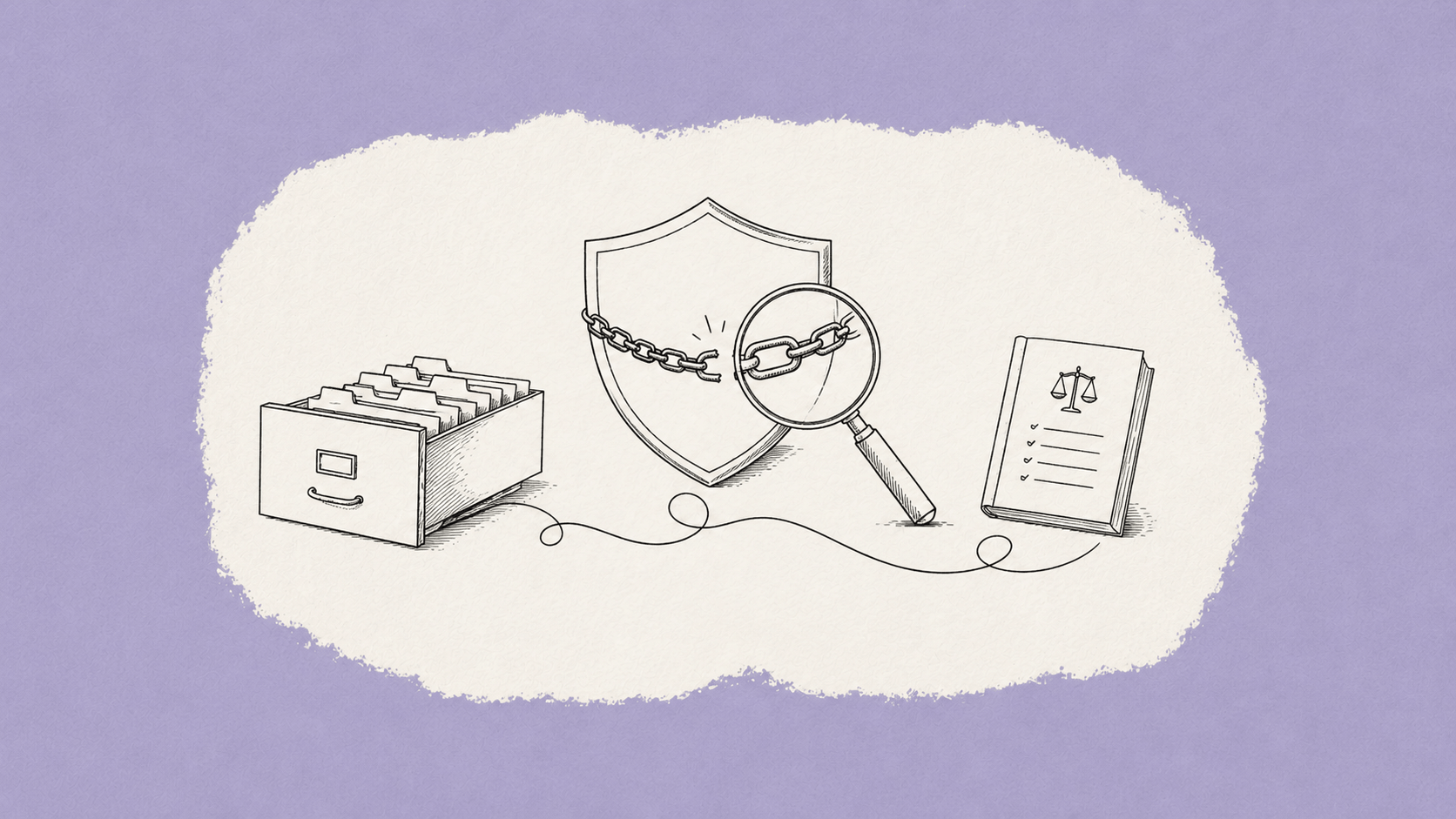

Industry-leading data security, for total peace of mind

We are a listed public company; currently protecting data for many of the world’s biggest professional brands.